Analyzing India's Quick Commerce War, 2026

The Indian quick commerce sector has evolved from a race for pure speed into a brutal war for sustainable unit economics.

While pioneer platforms built massive micro-fulfillment footprints, late-entrant Flipkart Minutes is radically shifting the narrative by prioritizing Average Order Value (AOV) over sheer store counts. This deep-dive analysis unpacks the metrics, strategies, and economic shifts shaping the hyperlocal delivery market in 2026.

The New Playbook of India's Quick Commerce Market

For years, the consensus around India’s hyper-competitive $11.5 billion quick commerce market was simple: first-mover advantage is everything. Platforms like Blinkit and Zepto aggressively burnt capital to secure prime real estate for dark stores, capturing dominant market shares across major metropolitan areas.

However, mid-2026 has brought a massive paradigm shift. The industry is realizing that scale without profitability is just noise. As the market matures, the ultimate metric of survival has pivoted from "How fast can you deliver?" to "How profitably can you scale?"

Enter Flipkart Minutes. Despite entering the 10-minute delivery ring late, the Walmart-backed e-commerce titan is demonstrating a calculated counter-strategy. Instead of chasing Blinkit's massive store count, Flipkart Minutes is focusing heavily on maximizing Average Order Value (AOV) and perfecting local unit economics.

The Data: How the Quick Commerce Giants Stack Up

To understand how Flipkart Minutes plans to redefine the economics of instant delivery, we must analyze the key operational metrics across the big four players.

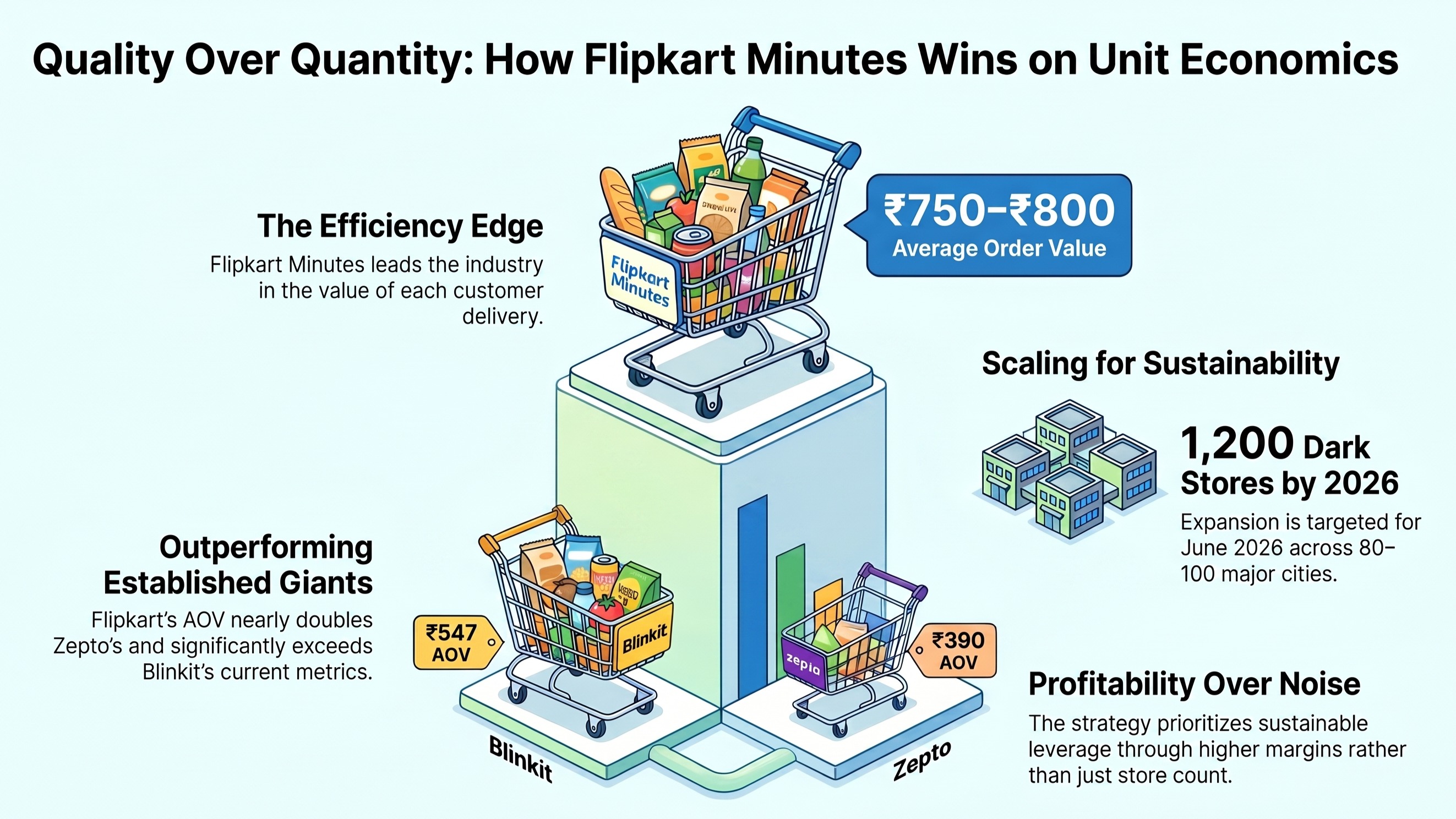

Blinkit: Operates 2,027 active dark stores across approximately 200 cities, maintaining an Average Order Value (AOV) of ₹547 with 1,200 daily orders per dark store.

Swiggy Instamart: Operates 1,136 active dark stores across 131 cities, maintaining an Average Order Value (AOV) of ₹746 with 1,034 daily orders per dark store.

Zepto: Operates 1,113 active dark stores across approximately 70 cities, maintaining an Average Order Value (AOV) of ₹390 while leading the group with 1,757 daily orders per dark store.

Flipkart Minutes: Currently operates 800 active dark stores across 80–100 cities, leading the industry with an Average Order Value (AOV) of ₹750–800 and bringing in 1,100 daily orders per dark store (with a target to expand to 1,200 dark stores by June 2026).

Cracking the Code: Why Average Order Value (AOV) Is the Ultimate Leverage

Zepto leads the industry in pure transactional velocity, pulling in an astonishing 1,757 daily orders per dark store. However, it struggles with a modest AOV of ₹390.

Blinkit maintains a balanced middle ground with 2,027 dark stores generating an average basket size of ₹547.

Flipkart Minutes leads the pack with an impressive AOV of ₹750–800, effectively tying with or outperforming Swiggy Instamart (₹746).

The Math Behind High-AOV Sustainability

In hyperlocal logistics, the cost of fulfillment, consisting of dark store rent, picking/packing labor, and rider payouts, remains largely fixed whether a delivery partner carries a ₹300 order or an ₹800 order.

When a platform maintains a lower AOV, it must rely heavily on volume and ad-revenue monetization to clear its operational break-even point. By consistently capturing a higher basket size (₹750+), Flipkart Minutes extracts significantly higher gross margins per delivery run. This creates immense economic leverage, allowing individual dark stores to achieve profitability much faster, even with fewer daily orders relative to Zepto.

Flipkart Minutes' Expansion Strategy: Speeding Up the Physical Footprint

A common critique of Flipkart Minutes was its limited physical footprint. However, the e-commerce incumbent is rapidly shrinking that gap.

Flipkart Minutes currently operates 800 dark stores across 80–100 cities, while pulling in a highly respectable 1,100 daily orders per dark store. Far from stagnant, its infrastructure rollout is moving at an aggressive pace, targeting 1,200 dark stores by June 2026.

Targeting Beyond Metros: The Tier-2 Strategy:

Unlike early incumbents who saturated Tier-1 micro-markets, Flipkart is leveraging its pre-existing, massive supply chain ecosystem to anchor its quick commerce expansion. By pushing heavily into Tier-2 and Tier-3 urban clusters—where Walmart-backed Flipkart already boasts massive consumer trust and brand recall—the platform is acquiring high-value users at a fraction of the customer acquisition cost (CAC) paid by pure-play instant delivery startups.

Can a Late Entrant Win the Quick Commerce War?

The traditional e-commerce model was built on centralized warehousing and deferred gratification. Quick commerce, conversely, intercepts high-frequency purchases right at the neighborhood level.

Flipkart Minutes is successfully turning its late-mover status into an advantage by bypassing the initial trial-and-error phase that burdened its predecessors. It isn't just selling low-margin groceries; it is aggressively injecting high-margin categories like electronics accessories, beauty products, home appliances, and festive fashion into the 10-minute delivery window. This exact category mix is what keeps its AOV soaring above the industry average.

While Blinkit remains the runaway market leader by volume and network density, scale without financial health is vulnerable. By focusing squarely on superior unit economics, high basket sizes, and calculated geographical scaling, Flipkart Minutes is proving that the quick commerce race won't be won by whoever started first—it will be won by whoever builds a highly profitable, self-sustaining logistical engine at speed.

Can Flipkart Minutes beat Zepto and Blinkit?Why is Average Order Value important in quick commerce?Which quick commerce platform has the highest AOV?Flipkart Minutes expansion strategy June 2026

#QuickCommerce #FlipkartMinutes #Blinkit #Zepto #SwiggyInstamart #HyperlocalDelivery #UnitEconomics #StartupIndia #ECommerceGrowth #RetailInnovation #BusinessStrategy #SupplyChainLogistics #VCFunding